មាសកំពុងមើលឃើញពីការផ្លាស់ប្តូរទិសដៅខណៈពេលដែលមានកត្តាមួយចំនួនដែលជម្រុញឲ្យតម្លៃមាសមានការកើនឡើងមកវិញ

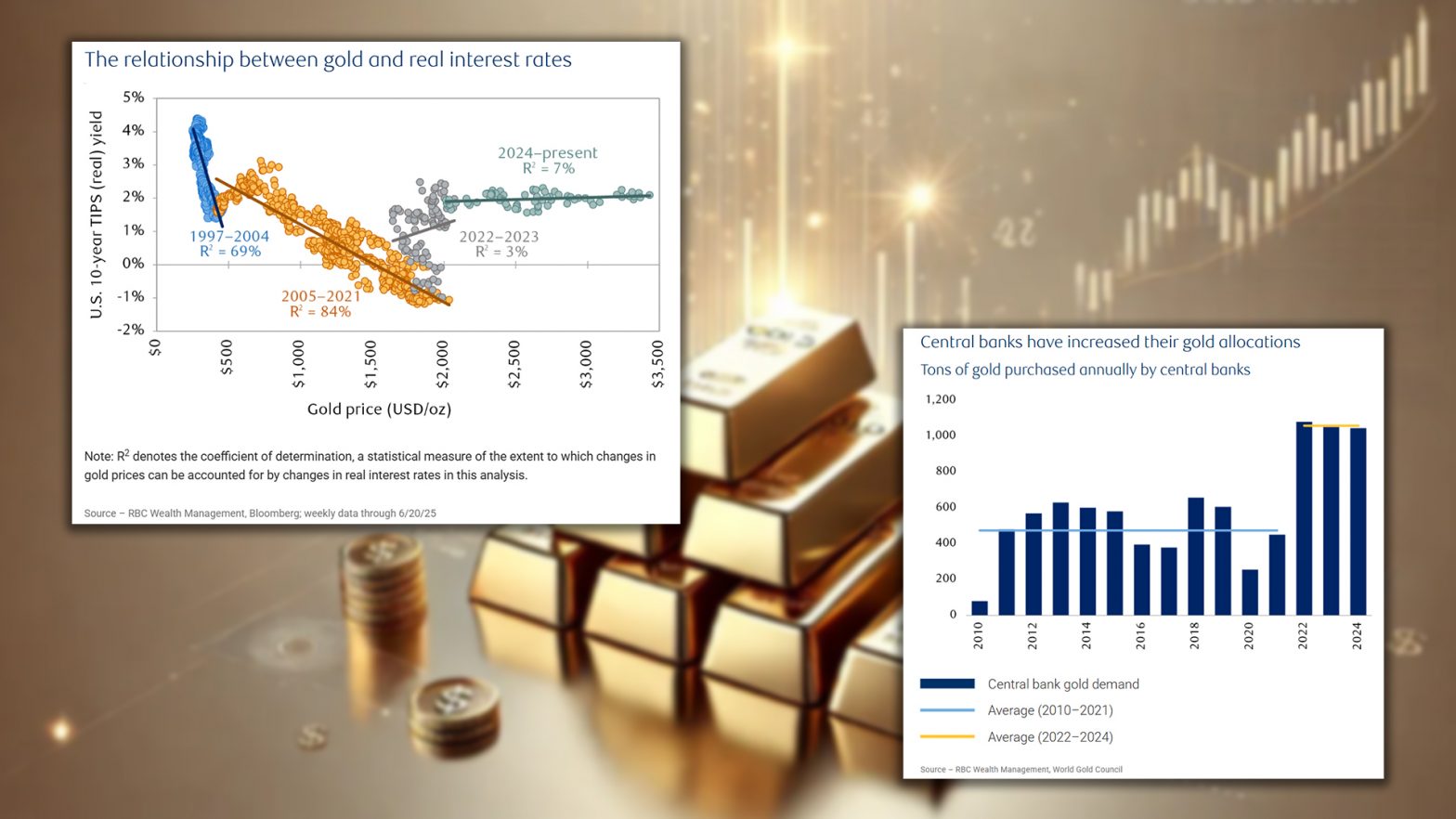

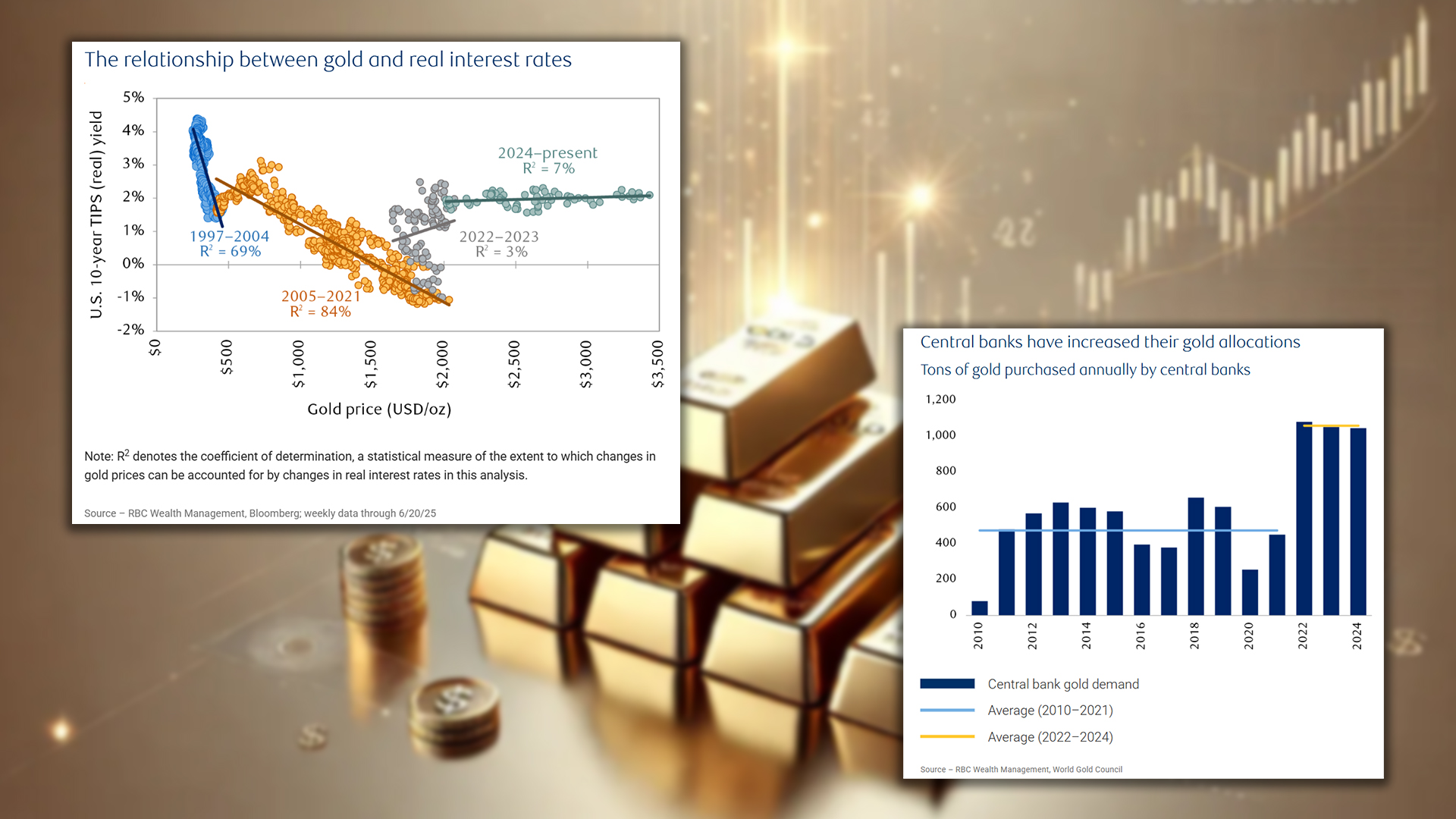

នៅក្នុងការវិភាគនាពេលថ្មីៗនេះ លោកJoseph Wu អនុប្រធាន និងជាអ្នកគ្រប់គ្រងផលប័ត្រនៅក្រុមហ៊ុន RBC Wealth Management ។ បាននិយាយថា ការកំណត់អត្តសញ្ញាណត្រឹមត្រូវនៃតម្លៃមាស តែងតែមានការលំបាក។ លោកបានបន្តថាទំនាក់ទំនងមួយដែលបានរក្សាបានយ៉ាងល្អក្នុងរយៈពេល 25 ឆ្នាំកន្លងមកគឺការជាប់ទាក់ទងគ្នារបស់មាសជាមួយនឹងអត្រាការប្រាក់ពិតប្រាកដ។ ចាប់ពីចុងទសវត្សរ៍ឆ្នាំ 1990 រហូតដល់ឆ្នាំ 2021 ការផ្លាស់ប្តូរនេះនៅតែមានស្ថេរភាព។ លោក Wu បាននិយាយថា “រយៈពេលនៃអត្រាការប្រាក់ទាប ឬធ្លាក់ចុះពិតប្រាកដវានឹងប៉ៈពាល់ទៅលើទិន្នផលសញ្ញាបណ្ណ័ជាតិរួមផ្សំទាំងការពារអតិផរណា – សន្តិសុខ – ជាធម្មតាអំណោយផលដល់បរិយាកាសអំណោយផលសម្រាប់មាស ។ ទោះជាយ៉ាងណាក៏ដោយចាប់តាំងពីឆ្នាំ 2022 លំនាំនេះបានចុះខ្សោយយ៉ាងខ្លាំង។ ទោះបីជាមានការកើនឡើងយ៉ាងខ្លាំងនៃអត្រាការប្រាក់ពិតប្រាកដក្នុងកំឡុងឆ្នាំ 2022 និង 2023 – ដោយសារធនាគារកណ្តាលបានដំឡើងអត្រាការប្រាក់យ៉ាងឆាប់រហ័សដើម្បីទប់ទល់នឹងអតិផរណាក្រោយជំងឺរាតត្បាត ទោះបីជាមានរឿងអ្វីកើតឡើងមាសនៅតែមានភាពធន់។ថ្មីៗនេះមាសបានឡើងថ្លៃបន្ថែមទៀត ទោះបីជាទិន្នផលពិតប្រាកដនៅតែថេរ។ មាសត្រូវបានគេមើលឃើញថាជាឃ្លាំងតម្លៃ ទ្រព្យសកម្មបម្រុងរបស់ធនាគារកណ្តាល និងអ្នកធ្វើពិពិធកម្មផលប័ត្រ។ លោក Wu បានកត់សម្គាល់ថា “តួនាទីដ៏ធំទូលាយនេះ បានបំបែកចេញពីគ្នាជាយូរណាស់មកហើយ ដែលទាមទារឱ្យមានក្របខ័ណ្ឌវិភាគផ្សេងគ្នា។ កម្លាំងជំរុញតម្រូវការជារឿយៗប្រែប្រួលអាស្រ័យលើផ្ទៃខាងក្រោយម៉ាក្រូទូលំទូលាយ។ ជាមួយនឹងទំនាក់ទំនងបញ្ច្រាសរវាងមាស និងអត្រាពិតប្រាកដធ្លាក់ចុះ លោក Wu បាននិយាយថា កត្តាកំណត់គន្លងរបស់មាសកំពុងផ្លាស់ប្តូរ។ លោក Wu បានកត់សម្គាល់ថាធនាគារកណ្តាលបានទិញដុំសុទ្ធជាង 1,000 តោនសម្រាប់រយៈពេល 3 ឆ្នាំជាប់ៗគ្នា – ទ្វេដងនៃមធ្យមភាគចន្លោះឆ្នាំ 2010 និង 2021 ដែលបានជួយទូទាត់តម្រូវការទន់ខ្សោយពីអ្នកវិនិយោគ។ គាត់បានសរសេរថា “និន្នាការនេះហាក់ដូចជានៅតែមាន: ការស្ទង់មតិថ្មីៗនេះនៃអាជ្ញាធររូបិយវត្ថុចំនួន 72 ដែលធ្វើឡើងដោយក្រុមប្រឹក្សាមាសពិភពលោកបានរកឃើញថាស្ទើរតែទាំងអស់ (95 ភាគរយ) នៃអ្នកឆ្លើយតបរំពឹងថានាឆ្នាំក្រោយពួកគេនឹងបន្ថែមចំនួនក្នុងការបង្កើនទុនបម្រុងរបស់ពួកគេ។ លោក Wu ជឿជាក់ថា លោហៈធាតុពណ៌លឿង គួរតែត្រូវបានគេមើលឃើញជាចម្បងថាជាការវិនិយោគរយៈពេលវែង។

Gold is witnessing a regime change as new factors drive bullion price

In a recent analysis, Joseph Wu, vice president and portfolio manager at RBC Wealth Management, said that accurately identifying the value of gold has always been difficult. He added that one relationship that has held up well over the past 25 years is gold’s correlation with real interest rates. From the late 1990s to 2021, this trend has remained stable. A period of low or falling real interest rates will affect bond yields, both as a hedge against inflation – a safe haven – usually conducive to a bullish environment for gold, Wu said. However, since 2022, this pattern has weakened significantly. Despite a sharp rise in real interest rates during 2022 and 2023 – as central banks quickly raised rates to combat inflation after the pandemic – gold has remained resilient. Recently, gold has rallied further even as real yields have remained flat. Gold is seen as a store of value, a central bank reserve asset and a portfolio diversifier. “These broad roles have long been separated, requiring different analytical frameworks,” Wu noted. The driving forces for demand often vary depending on the broader macro backdrop. With the inverse relationship between gold and falling real rates, Wu said the factors determining gold’s trajectory are changing. Wu noted that the central bank has bought more than 1,000 tons of gold for three consecutive years – double the average between 2010 and 2021 – which has helped offset weak demand from investors. “This trend appears to be continuing: a recent survey of 72 monetary authorities conducted by the World Gold Council found that almost all (95 percent) of respondents expect to add to their reserves next year, he wrote. Wu believes the yellow metal should be viewed primarily as a long-term investment.

——————-

📣 សម្រាប់ព័ត៌មានបន្ថែមសូមទំនាក់ទំនងតាមរយៈលេខតេឡេក្រាម

☎️ +855 81 734676

#FxInsights #FinancialNews #MarketUpdates #BreakingNewsUpdates

Recent News

Y.A.I Trading Co.,Ltd is registered in Cambodia with its registered office at Exchange Square, 14th Floor, Street 106, Sangkat Wat Phnom, Khan Daun Penh, Phnom Penh, Cambodia. Derivative Broker License No. 033

Phone: +855 99 777 495 | Email: info@yaitrading.com.kh

CFDs are complex financial instruments traded on margin. Trading CFDs carries a high level of risk and may not be suitable for all investors. Please ensure that you understand the risks involved as you may lose all your invested capital. Past performance of CFDs is not a reliable indicator of future performance. Most CFDs have no set maturity date and a CFD position matures on the date an open position is closed. Please read our ‘Risk Disclosure Notice’. When trading CFDs with YAI, you are merely trading on the outcome of a financial instrument and therefore do not take delivery of any underlying instrument, nor are you entitled to any dividends payable or any other benefits related to the same.

Y.A.I Trading Co.,Ltd does not offer Contracts for Difference to residents out of Cambodia.

Copyright © 2022 yaitrading.com.kh. All rights reserved